IPSASB SRS Exposure Draft 1, Climate-related Disclosures

Climate change affects everyone, transcending borders and economic boundaries. Rapid progress on climate change requires public sector action, and effective action requires the quality information only sustainability reporting standards specific to the sector’s needs can provide.

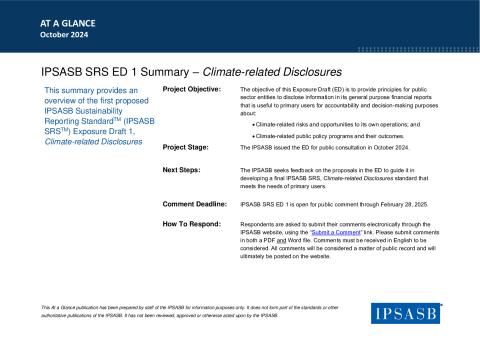

The IPSASB’s inaugural Sustainability Reporting Standards Exposure Draft (IPSASB SRS ED) 1, Climate-related Disclosures proposes disclosure requirements for public sector entities to report on (i) the climate-related risks and opportunities to its own operations and (ii) climate-related public policy programs and their outcomes, that are useful for primary users of general purpose financial reports to support decision-making and accountability.

These proposals align public sector reporting with global best practices, building on other international sustainability standards, while addressing the unique differences and information needs of primary users of public sector reports. This leads to more consistent, comparable and verifiable information across sectors to enable better decision-making and accountability, and maintaining access to funding needed for development, including from capital markets.

IPSASB standards are designed for public sector entities that meet the following three criteria:

- Are responsible for the delivery of services (encompassing goods, services and policy advice, including to other public sector entities) to benefit the public and/or to redistribute income and wealth;

- Mainly finance their activities, directly or indirectly, by means of taxes and/or transfers from other levels of government, social contributions, debt or fees; and

- Do not have the primary objective to make profits.

This includes a wide range of public sector entities, such as:

- National, regional, state/provincial and local governments;

- Government ministries, departments, programs, boards, commissions, agencies;

- Public sector social security funds, trusts and statutory authorities; and

- International governmental organizations.

SRS ED 1 is open for public comment until February 28, 2025. Comments must be submitted in English.

Feedback received on SRS ED 1 will shape the final standard which will assist governments and other public sectors around the world in responding to addressing climate change.

An At-a-Glance summary document, webcast, and brochure related to the draft can be found below. The brochure is available in English, Arabic, and Spanish.

Submitted Comment Letters

-

Public Sector Accounting Standards Board (PSASB) (410.4 KB)(Kenya)

-

Manulife Investment Management (MIM) (278.48 KB)(Canada)

-

Public Accountants and Auditors Board (PAAB) (760.94 KB)(Zimbabwe)

-

Principles for Responsible Investment (PRI) (425.83 KB)(- International)

-

South African Institute of Chartered Accountants (SAICA) (448.4 KB)(South Africa)

-

Ministry of Finance of the Republic of Poland (358.19 KB)(Poland)

-

Association of Chartered Certified Accountants (ACCA) and Pan African Federation of Accountants (PAFA) (308.81 KB)(- International)

-

Comissão de Normalização Contabilística (CNC) (377.76 KB)(Portugal)

-

Forvis Mazars Group SC (287.11 KB)(France)

-

Deloitte Global (228.81 KB)(- International)

-

Conselho Federal de Contabilidade (CFC) (626.11 KB)(Brazil)

-

First Nations Financial Management Board (FMB) (142.69 KB)(Canada)

-

National Board Of Accountants And Auditors (NBAA) (286.43 KB)(Tanzania, United Republic of)

-

Board of Deans of Colleges of Public Accountants of Peru (484.79 KB)(Peru)

-

Forum of Governmental Accounting of Latin America (FOCAL) (1.09 MB)(Chile)

-

Forum of Governmental Accounting of Latin America (FOCAL) (1.09 MB)(Colombia)

-

Forum of Governmental Accounting of Latin America (FOCAL) (1.09 MB)(Ecuador)

-

Forum of Governmental Accounting of Latin America (FOCAL) (1.09 MB)(El Salvador)

-

Forum of Governmental Accounting of Latin America (FOCAL) (1.09 MB)(Guatemala)

-

Forum of Governmental Accounting of Latin America (FOCAL) (1.09 MB)(Panama)

-

Forum of Governmental Accounting of Latin America (FOCAL) (1.09 MB)(Peru)

-

Forum of Governmental Accounting of Latin America (FOCAL) (622.12 KB)(Dominican Republic)

-

Office of the Auditor General of Ontario (228.38 KB)(Canada)

-

City of Mississauga (113.33 KB)(Canada)

-

Kalar Consulting Ltd (564.08 KB)(United Kingdom)

-

Auditor General of Canada (OAG) (337.61 KB)(Canada)

-

The Regional Partnership for the promotion of sustainability and SDG reporting in Latin America (LAP) (620.7 KB)(- International)

-

Natalie Rulloda (207.12 KB)(Portugal)

-

Kris Kauffmann (43.29 KB)(Australia)

-

KPMG LLP (199.25 KB)(Canada)

-

Welch LLP (177.22 KB)(Canada)

-

Özge Selçuk (381.61 KB)(Türkiye)

-

Norwegian Organization for Local Government Control and Auditing (NKRF) (177.88 KB)(Norway)

-

Cour des comptes (1.71 MB)(France)

-

Brazilian Integrated Reporting Commission (CBARI) (322.66 KB)(Brazil)

-

International Standards of Accounting and Reporting (ISAR) (207.29 KB)(- International)

-

The World Bank (272.64 KB)(- International)

-

Conseil de Normalisation des Comptes Publics (CNoCP) (715.26 KB)(France)

-

McGuinness Institute (2.9 MB)(New Zealand)

-

Institute of Chartered Accountants of India (ICAI) (296.54 KB)(India)

-

Public Sector Accounting Board (PSAB) (301.5 KB)(Canada)

-

Accounting Standards Board (ASB) (276.98 KB)(South Africa)

-

Ministry of Finance (1003.48 KB)(Saudi Arabia)

-

Ministry of Finance (2) (1003.48 KB)(Saudi Arabia)

-

Ministry of Finance (3) (1003.48 KB)(Saudi Arabia)

-

Ministry of Finance (4) (1003.48 KB)(Saudi Arabia)