IPSASB SRS Exposure Draft 1, Climate-related Disclosures

Climate change affects everyone, transcending borders and economic boundaries. Rapid progress on climate change requires public sector action, and effective action requires the quality information only sustainability reporting standards specific to the sector’s needs can provide.

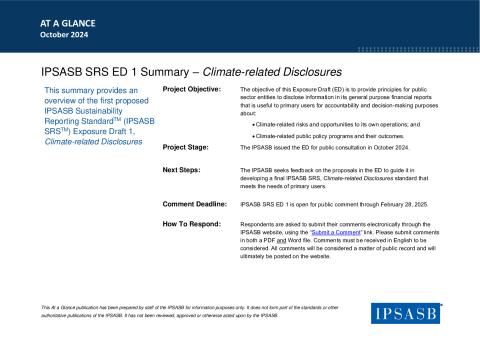

The IPSASB’s inaugural Sustainability Reporting Standards Exposure Draft (IPSASB SRS ED) 1, Climate-related Disclosures proposes disclosure requirements for public sector entities to report on (i) the climate-related risks and opportunities to its own operations and (ii) climate-related public policy programs and their outcomes, that are useful for primary users of general purpose financial reports to support decision-making and accountability.

These proposals align public sector reporting with global best practices, building on other international sustainability standards, while addressing the unique differences and information needs of primary users of public sector reports. This leads to more consistent, comparable and verifiable information across sectors to enable better decision-making and accountability, and maintaining access to funding needed for development, including from capital markets.

IPSASB standards are designed for public sector entities that meet the following three criteria:

- Are responsible for the delivery of services (encompassing goods, services and policy advice, including to other public sector entities) to benefit the public and/or to redistribute income and wealth;

- Mainly finance their activities, directly or indirectly, by means of taxes and/or transfers from other levels of government, social contributions, debt or fees; and

- Do not have the primary objective to make profits.

This includes a wide range of public sector entities, such as:

- National, regional, state/provincial and local governments;

- Government ministries, departments, programs, boards, commissions, agencies;

- Public sector social security funds, trusts and statutory authorities; and

- International governmental organizations.

SRS ED 1 is open for public comment until February 28, 2025. Comments must be submitted in English.

Feedback received on SRS ED 1 will shape the final standard which will assist governments and other public sectors around the world in responding to addressing climate change.

An At-a-Glance summary document, webcast, and brochure related to the draft can be found below. The brochure is available in English, Arabic, and Spanish.

Submitted Comment Letters

-

City of London Corporation (117.53 KB)(United Kingdom)

-

The New York State Society of Certified Public Accountants (NYCPA) (221.24 KB)(United States of America)

-

EEE Sustainability Advisors Limited (49.95 KB)(United Arab Emirates)

-

Altaf Noor Ali (1.05 MB)(Pakistan)

-

Railpen (184.16 KB)(United Kingdom)

-

Institute of Certified Public Accountants of Kenya (ICPAK) (320.24 KB)(Kenya)

-

International Corporate Governance Network (ICGN) (201.09 KB)(- International)

-

Province of British Columbia (241.17 KB)(Canada)

-

North Atlantic Treaty Organization (NATO) (232.22 KB)(- International)

-

World Meteorological Organization (WMO) (167.98 KB)(- International)

-

Malaysian Institute of Accountants (MIA) (489.03 KB)(Malaysia)

-

Mo Chartered Accountants (133.38 KB)(Zimbabwe)

-

Korea Institute of Public Finance (KIPF) (272.06 KB)(Korea)

-

Swiss Public Sector Financial Reporting Advisory Committee (SRS-CSPCP) (183.83 KB)(Switzerland)

-

United Nations - World Food Programme (WFP) (240.53 KB)(- International)

-

Dr Xinwu He (93.02 KB)(United Kingdom)

-

GSG Impact & Social Value International (424.01 KB)(- International)

-

Australasian Council of Auditors-General (ACAG) (464.37 KB)(- International)

-

Training and Advisory Services Chartered Accountant (TAS) and Chartered Accountants Academy (CAA) (207.27 KB)(Zimbabwe)

-

Government of Jersey (146.13 KB)(Jersey)

-

European Accounting Association Public Sector Accounting Committee (EAA PSAC) (168.01 KB)(- International)

-

United Nations (188.98 KB)(- International)

-

Cities of Calgary, Edmonton, Montreal, Toronto, and Vancouver (591.21 KB)(Canada)

-

Chartered Institute of Public Finance and Accountancy (CIPFA) and Institute of Chartered Accountants in England and Wales (ICAEW) (216.47 KB)(United Kingdom)

-

CDP (146.02 KB)(- International)

-

University Pension Plan (UPP) (152.63 KB)(Canada)

-

INTOSAI Development Initiative (IDI) (94.02 KB)(- International)

-

HM Treasury (HMT) (305.84 KB)(United Kingdom)

-

Organismo Italiano Business Reporting (O.I.B.R.) (319.4 KB)(Italy)

-

Wayne Morgan Byron Ofner (87.58 KB)(Canada)

-

External Reporting Board (XRB) (430.46 KB)(New Zealand)

-

Chartered Accountants Australia and New Zealand (CA ANZ) and CPA Australia (236.41 KB)(- International)

-

The Japanese Institute of Certified Public Accountants (JICPA) (411.64 KB)(Japan)

-

The New Zealand Treasury (265.99 KB)(New Zealand)

-

The Heads of Treasuries Accounting and Reporting Advisory Committee (HoTARAC) (169.46 KB)(Australia)

-

PricewaterhouseCoopers International (242.63 KB)(- International)

-

Jens Heiling, Lars Tanzmann, Helge Brixner (117.59 KB)(Germany)

-

Institute of Certified Public Accountants of Uganda (ICPAU) (272.52 KB)(Uganda)

-

Agency for Public Finance and Management (164.75 KB)(Denmark)

-

Accountancy Europe (226.89 KB)(- International)

-

Financial Reporting Council of Nigeria (FRC) (237.21 KB)(Nigeria)

-

UK National Audit Office (303.84 KB)(United Kingdom)

-

MSCI ESG Research LLC (142.76 KB)(United States of America)

-

Institute Of Chartered Accountants, Ghana (271.72 KB)(Ghana)

-

Global Reporting Initiative (GRI) (315.24 KB)(- International)

-

Commission on Audit (COA) (268.44 KB)(Philippines)

-

Institut der Wirtschaftsprüfer in Deutschland e.V. (IDW) (136.97 KB)(Germany)

-

Rethinking Capital (277.52 KB)(United Kingdom)

-

SAI Indonesia (167.62 KB)(Indonesia)

-

African Association of Accountants General (AAAG) (484.38 KB)(- International)