CURRENT STATUS OF THE PROJECT

The IPSASB approved the final pronouncements IPSAS 50, Exploration for and Evaluation of Mineral Resources, and Stripping Costs in the Production Phase of a Surface Mine (Amendments to IPSAS 12). These new pronouncements provide guidance for public sector entities operating in extractive industries, with accounting guidance aligned with the private sector. They will be effective from January 1, 2027 with early adoption permitted, and are expected to be published in Q4 2024.

Image

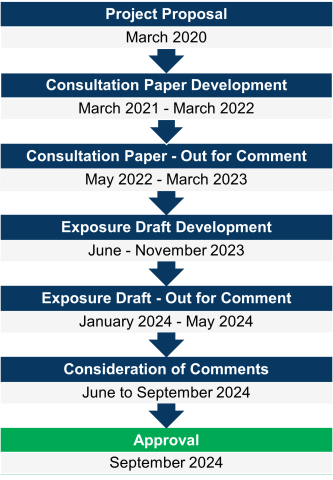

PROJECT TIMELINE

The project timeline is depicted below. Please note that these are current targeted milestones/phases and may change as the work in this area progresses.

PROJECT OVERVIEW

Objective

This project originated from the Natural Resources project. The IPSASB decided to separate the development of IFRS 6 and IFRIC 20 aligned guidance due to the specific nature of these accounting areas. The objective of this project is to propose:

- Financial reporting for the exploration for and evaluation of mineral resources. This includes the measurement, presentation and disclosure requirements for exploration and evaluation assets recognized by applying the entity’s accounting policy to capitalize exploration and evaluation expenditure. The IPSASB adopted the existing private sector requirements in IFRS 6, Exploration for and Evaluation of Mineral Resources.

- Guidance to account for the benefits that may arise from the waste removal activity of a surface mine. This waste removal activity is known as ‘stripping’. The IPSASB adopted the existing private sector requirements in IFRIC 20, Stripping Costs in the Production Phase of a Surface Mine.

Why the IPSASB Undertook this Project

During its consultation on the project for Natural Resources, the IPSASB identified a need for specific guidance to be issued to entities in the public sector who are involved in the exploration for and extraction of mineral resources.

No specific public sector accounting guidance currently exists for accounting for exploration and evaluation expenditure, or stripping costs.

To address potentially diverse accounting practice, the IPSASB considered it important to develop this guidance for improved accountability and comparability purposes.

Consultation

The IPSASB approved ED 86 and ED 87 at the December 2023 IPSASB meeting, issued for public comment in January 2024, with the comment period closing on May 31, 2024

Limited changes were made to IFRS 6 (ED 86) and IFRIC 20 (ED 87).

Project Contact

Published Documents and Support

Documents in this section include:

- Major documents published by the IPSASB during the lifecycle of the project including: Consultation Papers, Exposure Drafts, issued IPSAS, amendments to IPSAS, and other similar due process documents;

- Supporting material related to each published document including: snapshots, webinars, and other material; and

- The project-relevant IPSASB agenda papers.

Content

Summary

Summary

Included in this section are documents related to the development of the Consultation Paper.

Content

Content

Content

Content